What are the 3 credit bureaus and why do they matter?

The three major credit bureaus — Experian, Equifax, and TransUnion — collect financial information that lenders use to assess your creditworthiness. Learn more about each bureau, including how they work and how they calculate credit scores. Then get a personal finance app to help monitor your credit, cut costs, and boost savings.

2025

PCMag

60X Winner

A credit bureau is a company that collects and manages financial data, including your borrowing and repayment history. The three major credit bureaus — Experian, Equifax, and TransUnion — handle over 1.6 billion credit accounts between them.

These bureaus play an important role in managing your credit report and score, impacting your ability to secure loans, get favorable interest rates, and even rent certain apartments. Understanding how the three credit bureaus work can help you better grasp their roles in shaping your credit.

Keep reading to learn more about the three largest credit bureaus and why they matter for your finances.

1. Experian

Experian, headquartered in Dublin, Ireland, began in 1826 when London merchants started sharing information on customers with unpaid debts. The bureau was officially formed in 1996, when the U.K. business and the U.S. business, previously known as TRW, merged.

2. TransUnion

TransUnion, headquartered in Chicago, Illinois, was originally formed in 1968 as a holding company for Union Tank Car Company. It entered the credit reporting industry in 1969 by acquiring the Credit Bureau of Cook County, and it has since grown into a global provider of credit information and risk management services.

3. Equifax

Equifax, headquartered in Atlanta, Georgia, was founded in 1899 by the brothers Cator and Guy Woolford as the Retail Credit Company. It initially collected consumer data for insurance companies and transitioned into a credit bureau by expanding its services to include credit reporting and financial information.

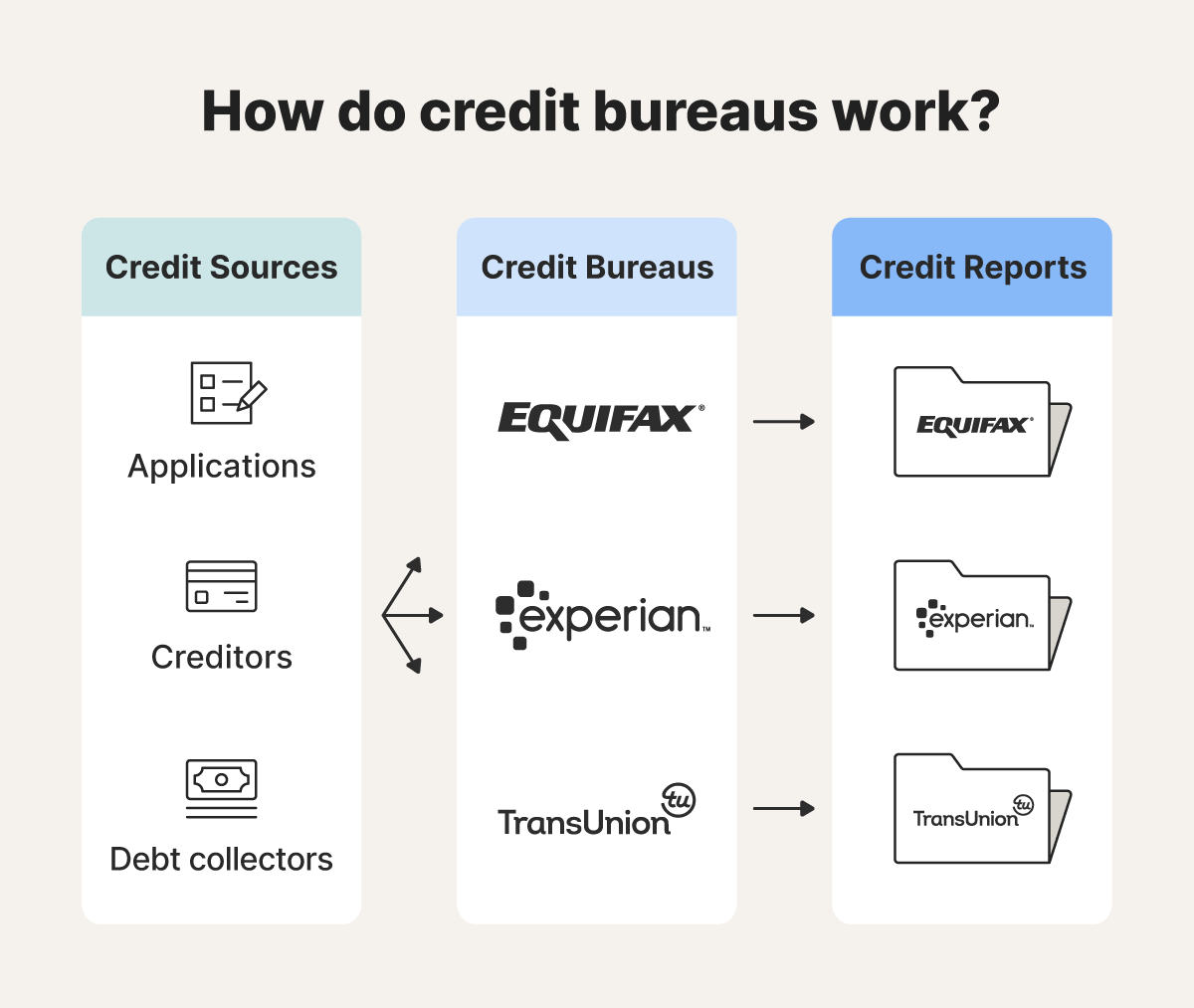

How do credit bureaus work?

Credit bureaus gather, store, and share consumer information with authorized parties to help assess your likelihood of repaying borrowed money or meeting financial obligations.

Using the financial data they collect, credit bureaus create your credit report and calculate your credit score. These tools help lenders, landlords, and other entities evaluate your financial responsibility.

Most of the information credit bureaus collect comes from companies like:

- Financial institutions

- Credit card issuers

- Mortgage lenders

- Utility companies

- Debt collection agencies

Additionally, credit bureaus gather information from public records, like bankruptcies, foreclosures, and tax liens, which can also impact your credit score.

While credit bureaus provide information to help assess creditworthiness, they do not make lending decisions. It’s up to individual entities to decide whether to approve or deny an application.

What information do credit bureaus collect?

Credit bureaus collect financial and personal information — like your address, Social Security number, and payment history — to create a detailed picture of your credit profile.

Information credit bureaus collect include:

- Personal information: Your name, date of birth, Social Security number, current and past addresses, and employment history.

- Credit accounts: Details about loans, credit cards, mortgages, and other credit accounts, including account types, balances, payment history, and credit limits.

- Payment history: Records of on-time and missed payments for credit accounts and utility bills.

- Public records: Information from court filings, such as bankruptcies, foreclosures, or tax liens.

- Debt collection activity: Details about accounts sent to collections and their current status.

- Credit inquiries: A record of when lenders, landlords, or other authorized parties check your credit report.

How do credit bureaus calculate your credit score?

While all three credit bureaus use similar factors to calculate your score, their factor weighting and calculation methods are different; therefore, your credit score may differ from bureau to bureau. Additionally, not all businesses report to every bureau, which can lead to variations.

Let's take a closer look at how each bureau calculates its credit score:

Equifax credit score

Unlike the other major bureaus, Equifax uses an independent scoring system with scores ranging from 280 to 850. Unlike other credit scoring models, Equifax does not disclose the exact weight it places on different factors that impact your score.

TransUnion credit score

TransUnion provides credit scores based on the VantageScore 3.0 model, which ranges from 300 to 850. This credit scoring model places a greater emphasis on payment history and credit mix than the FICO scoring model used by Experian.

Here's how the VantageScore 3.0 model weighs factors impacting your credit.

- Payment history (40%)

- Age and credit mix (21%)

- Credit utilization (20%)

- Balance (11%)

- New credit (5%)

- Available credit (3%)

Experian credit score

Experian also uses the FICO scoring model, with a credit range from 300 to 850. However, their use of the scoring model places a greater emphasis on credit utilization than the VantageScore model.

Here’s a breakdown of FICO credit score factors:

- Payment history (35%)

- Credit utilization (30%)

- Credit age (15%)

- Credit mix (10%)

- Number of inquiries (10%)

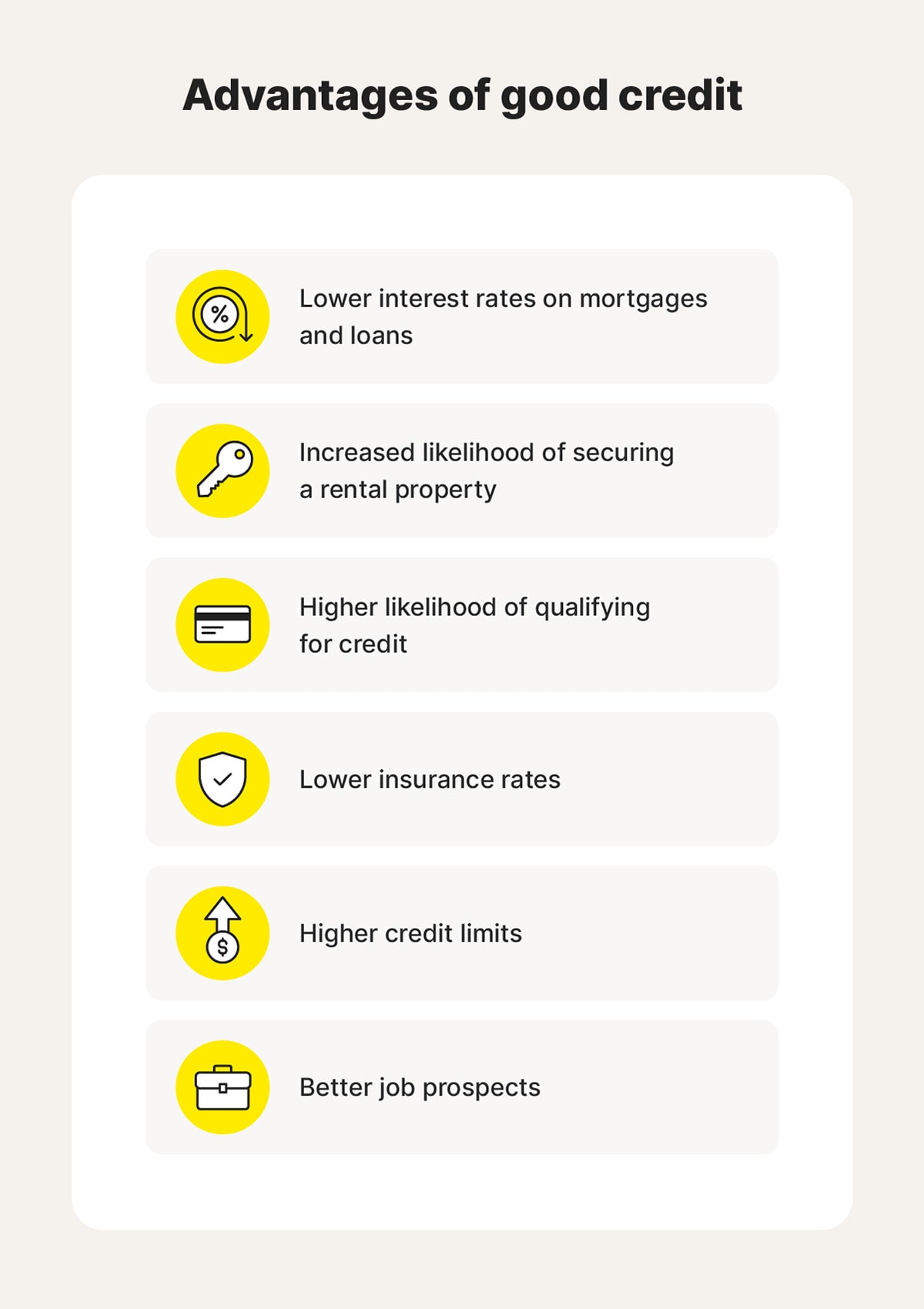

Why are credit bureaus important for your financial health?

Your credit score and credit report carry a lot of weight for many of life’s milestones. From securing a mortgage to getting approved for a car loan or even landing certain jobs, having good credit makes it easier to achieve your goals.

Credit bureaus collect and maintain information about your financial behavior, which is used to calculate your credit score and inform your credit report. Depending on how responsibly you manage credit, this information can either open or close doors to financial opportunities.

Here’s how your credit score can influence your financial opportunities:

- Interest rates on loans: Higher credit scores often qualify you for lower interest rates, saving you money on mortgages, auto loans, and personal loans.

- Ability to secure a rental property: Landlords may check your credit to determine if you’re a reliable tenant. Poor credit could affect your chances of approval.

- Ability to qualify for credit: A good credit score makes it easier to get approved for credit cards, loans, and lines of credit.

- Insurance rates: Some insurance providers use credit scores to help determine your premiums, meaning better credit could lead to lower rates.

- Credit limits: Lenders may offer higher credit limits to borrowers with strong credit histories, providing more financial flexibility.

- Job prospects: Certain employers may review credit reports as part of the hiring process, particularly for jobs that involve financial responsibilities.

How to contact all three credit bureaus

If your credit score is lower than expected, it could signal a larger issue with your credit report. Errors on your credit report can range from simple mistakes to more serious issues like identity theft. If you spot an error, contact the credit bureaus and dispute the mistake. This helps ensure your credit file accurately reflects your financial situation.

Below is the contact information for each credit bureau:

Equifax |

Experian |

TransUnion |

|---|---|---|

(888) 378-4329 |

(855) 414-6048 |

(800) 680-7289 |

Equifax Information Services LLC |

Experian |

TransUnion Consumer Solutions |

Control your financial health

Understanding how the three major credit bureaus impact your financial health is one small step toward building a stronger credit score. Norton Money helps you stay informed with credit score tracking and visibility into key changes across your credit profile — giving you clearer insight into your financial health and greater confidence in the decisions you make.

FAQs

Which credit bureau is best?

All three credit bureaus report financial data accurately, so there isn't necessarily a “best” bureau. However, knowing which bureau most of your lenders report to can help you get a more accurate picture of your credit score.

Can you dispute credit report errors?

You can and should dispute credit report errors. To dispute a credit report error, reach out to the credit bureau directly and follow their dispute process.

How can you get a free credit report?

You’re entitled to a free credit report each year from each of the three major credit bureaus. While those reports show your full credit history, Norton Money helps you stay informed between reports by tracking your credit score and alerting you to key changes.

Editors' note: Our articles offer educational information and are written to raise awareness about important topics in Cyber Safety. Norton products and services may not protect against every type of threat, fraud, or crime we write about. For more details about how we research, write, and review our articles, see our Editorial Policy.

Want more?

Follow us for all the latest news, tips, and updates.