How and when to withdraw from your 401(K)

A 401(k) is an employer-sponsored retirement savings account that allows you to invest pre-tax income for long-term growth. Read on to learn when and how to withdraw from your 401(k). Then, get a secure financial wellness app to help you better manage your money and plan for retirement.

2025

Consumer

Security Innovator

A 401(k) is a common retirement saving plan, and understanding when and how to withdraw from it is crucial for optimizing your retirement earnings. While withdrawing funds early may be necessary during financial hardship, there are serious risks. Knowing 401(k) withdrawal rules and penalties can help you make more informed decisions about your money.

This article discusses withdrawals from a traditional 401(k). Withdrawal rules for Roth 401(k) accounts are different and are not covered here.

Ways to withdraw money from a 401(k) account

If you’re 59½ or older, simply contact your plan administrator to start withdrawing from your 401(k) without the 10% early-withdrawal penalty. Just remember that withdrawals from a traditional 401(k) are taxed as ordinary income.

If you can’t wait until you turn 59½, there are other options for taking money out of a 401(k) that you can consider. These include hardship withdrawals for urgent expenses, taking a 401(k) loan to repay over time, or using substantially equal periodic payments (SEPP) to avoid the 10% early withdrawal penalty if IRS rules are met.

Read on to learn about the different types of withdrawals, their rules, downsides, and how to access them if necessary. We’ve covered the following options, in order of safest to riskiest:

- 401(k) loan.

- Substantially equal periodic payments (SEPP).

- Hardship withdrawal.

- Standard early withdrawal.

- Cancel 401(k) and cashout.

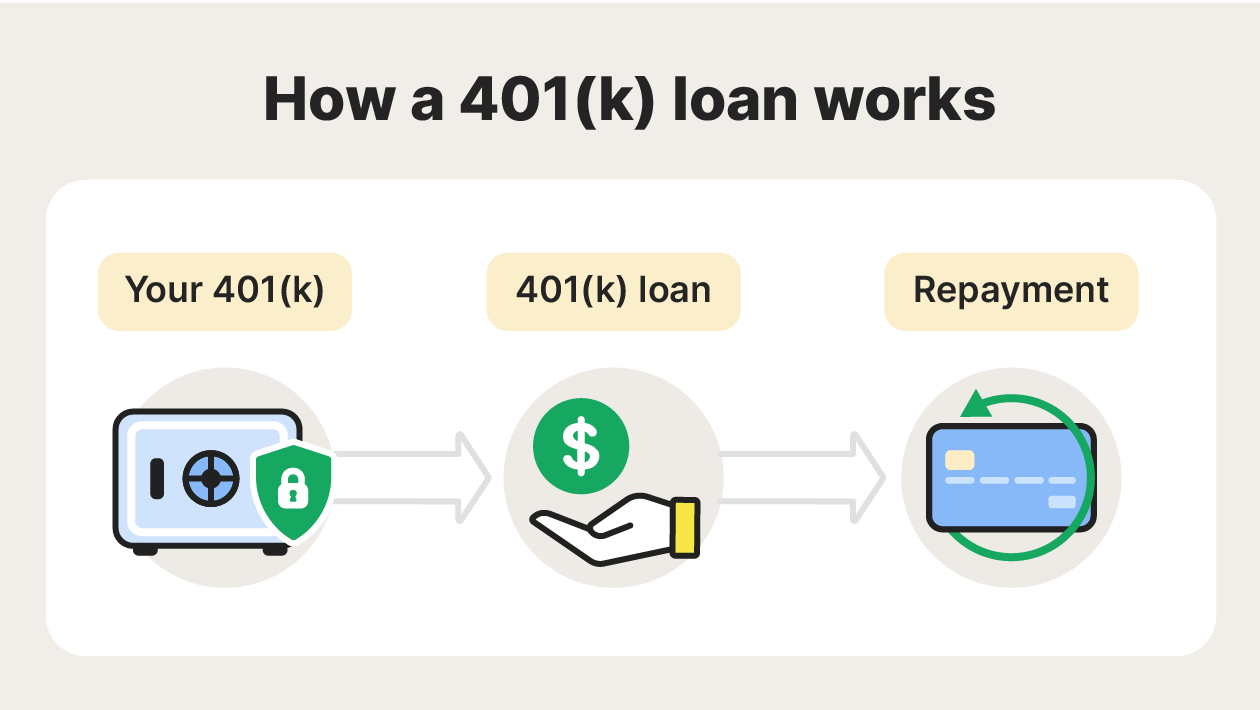

A 401(k) loan allows you to borrow money from your retirement account, typically up to $50,000 or 50% of your vested balance, whichever is less. Unlike a withdrawal, which removes funds permanently, a loan allows you to repay the borrowed amount, plus interest, over time, usually within five years. The interest you pay on your loan goes directly into your account, not to your bank or plan provider.

Here’s how to take out a 401(k) loan:

- Check your loan eligibility: Review your plan’s rules. Some plans may not offer loans.

- Request the loan: Contact your plan administrator to complete the necessary paperwork, which typically includes specifying the amount and repayment terms.

- Wait for loan approval: If approved, funds are distributed to you, and you begin repaying them according to your plan’s schedule.

What you need to know

A 401(k) loan offers a relatively quick way to access funds without the tax penalties associated with a withdrawal.

Withdrawals typically incur income taxes and a 10% early withdrawal penalty, meaning you require a larger amount of money to cover the same need. Loans, on the other hand, avoid immediate tax implications. Also, your loan payments and interest go back into your account, making 401(k) loans an attractive option for covering short-term financial needs like medical expenses or home repairs.

Risks of a 401(k) loan

Borrowing from your 401(k) carries several risks:

- If you leave your job before repaying the loan, you typically have until your tax return due date to repay the balance and any unpaid amount will be subject to taxes and penalties. This applies to both traditional and Roth 401(k)s.

- The borrowed funds are no longer invested, meaning you miss out on potential returns, which could reduce your final retirement savings balance.

Top tip: Before taking a 401(k) loan, weigh the long-term impact on your retirement savings and consider whether other loan options, such as personal loans or home equity lines of credit (HELOC), might be more suitable.

Substantially equal periodic payments (SEPP) is a withdrawal method that allows you to take early distributions from your retirement account without the typical 10% early withdrawal penalty, as long as you follow specific IRS guidance.

Under SEPP, you must take a series of substantially equal withdrawals over a set period, generally based on your life expectancy. Once started, these withdrawals must continue for at least five years or until you reach age 59½, whichever is longer. SEPP offers a steady income stream without early withdrawal penalties, making it an option for those retiring early.

Here’s how to withdraw from your 401(k) using SEPP:

- Consider rolling your 401(k) into an IRA first: Many people do this because IRAs usually offer more flexible payment options, while some 401(k) plans don’t support the fixed, ongoing withdrawal schedule that SEPP requires.

- Calculate your withdrawal amounts: Use one of three IRS-approved calculation methods:

- Required Minimum Distribution (RMD).

- Fixed Amortization.

- Fixed Annuitization.

- Set up your withdrawal schedule: Choose your payment frequency (annually, quarterly, or monthly) and begin taking regular, equal distributions according to your selected calculation method.

What you need to know

SEPP withdrawals are still taxed as ordinary income. The main advantage is that they avoid the 10% early withdrawal penalty. To use SEPP with a 401(k), you must be separated from the employer that sponsors the plan: you can’t start SEPP withdrawals while you’re still working for that company.

Remember that SEPP rules are strict. Unless you qualify for an exception, changing your payment amount or schedule before the required period ends will trigger the 10% penalty retroactively on all prior withdrawals, plus interest. This makes knowing how to set a budget key.

Risks of SEPP

Here are some of the risks associated with SEPP:

- Long-term commitment with severe penalties for breaking: Modifying your withdrawals before the required period ends triggers retroactive penalties on all distributions you’ve taken.

- Inflexibility if circumstances change: In most cases, you cannot adjust payment amounts if your financial situation improves or worsens.

- Reduced retirement savings: Regular withdrawals mean less money remains invested, reducing potential compound growth over time.

- Complex calculations: Errors in calculating SEPP amounts can result in IRS penalties.

- Strict payment schedule: You cannot skip payments or change their frequency once they’ve started.

Top tip: SEPP works best for people who need a reliable stream of income, starting before age 59½, and expect that it will need to last several years.

Because the rules are strict and mistakes can be costly, it’s important to work with a qualified financial advisor or tax professional to calculate payments correctly and set everything up properly. Even a small error can trigger retroactive penalties that add up quickly.

A hardship withdrawal from a 401(k) is defined by the IRS as access to funds early to meet an immediate and heavy financial need while still working.

Here’s how to take a hardship withdrawal from your 401(k):

- Confirm withdrawal eligibility: Review your 401(k) plan’s rules, as not all plans allow hardship withdrawals and there may be specific criteria.

- Gather proof of hardship: Provide evidence of your financial need, such as medical bills, a funeral invoice, or tuition statements. Use a 401(k) hardship withdrawal calculator to work out the precise withdrawal amount you need.

- Submit your request: Send your evidence and hardship application to your plan administrator.

- Withdrawal approval: If you qualify for hardship, the IRS requires your employer to approve your withdrawal request.

What you need to know

Hardship withdrawals are subject to income tax as well as the 10% early withdrawal penalty (unless you qualify for a separate penalty exemption). There are strict criteria you must meet, and you can only withdraw the amount you need to cover your financial emergency.

The following situations may qualify as financial hardship and can apply to both the account holder and their family members:

- Qualifying medical expenses.

- Funeral expenses.

- Higher education expenses.

- Expenses incurred from living or working in a federally declared natural disaster zone.

- Expenses to avoid eviction or foreclosure on your primary residence.

Your plan administrator will require “proof of need” and approval from your employer. Some plans may not allow for hardship withdrawals.

Hardship withdrawals are often treated as a “last resort” method as repayment is not required. While this option may seem attractive, especially in an emergency, it’s important to weigh the long-term effects that the withdrawal can have on your retirement planning.

Risks of hardship withdrawals

A hardship withdrawal from a 401(k) comes with significant risks:

- Permanent reduction in retirement savings: Withdrawn funds can’t be repaid, and you miss out on years of potential compound growth.

- Immediate tax liability: Withdrawals are taxed as ordinary income, which can increase your taxable income and potentially push you into a higher tax bracket.

- 10% early withdrawal penalty: Unless you qualify for a separate penalty exception, you’ll owe an additional 10% penalty on top of income taxes.

- Legal consequences for false claims: Claiming hardship when you don't have a legitimate need can result in serious penalties.

Top tip: Consult your plan administrator and a financial advisor before making a hardship withdrawal to ensure you meet the relevant criteria and minimize the impact on your future financial security.

A standard early withdrawal from a 401(k) is when you take money from your account before reaching the age of 59½. This typically results in having to pay income taxes on withdrawn funds plus a 10% early withdrawal penalty, though some exceptions apply.

People may choose early withdrawal after job loss, to cover emergency expenses, or to fund major life events. According to the Employment Benefit Research Institute, anywhere from a third to nearly half of 401(k) savers withdraw funds after a job change.

Here’s how to process an early withdrawal from your 401(k) account:

- Contact your 401(k) plan administrator: Request information about your plan's withdrawal options and any required documentation.

- Fill out the required forms: Specify the amount you wish to withdraw. Your plan administrator will provide the necessary paperwork.

- Understand the tax implications: Your plan will typically withhold 20% for federal taxes automatically, but you may owe more depending on your tax bracket and whether you qualify for penalty exceptions.

- Receive your funds: Processing typically takes several business days to a few weeks, depending on your plan.

What you need to know

The entire withdrawal amount is taxed as ordinary income, and you’ll owe a 10% early withdrawal penalty unless you qualify for an exception. Common penalty exceptions include:

- Unreimbursed medical expenses exceeding 7.5% of your adjusted gross income.

- Permanent disability.

- Leaving your job at age 55 or older.

- Qualified Domestic Relations Orders (A court order dividing retirement assets in a divorce).

- IRS levy on your plan.

The Rule of 55: If you leave your job (voluntarily or involuntarily) during or after the year you turn 55, you can take penalty-free withdrawals from that employer’s 401(k). Income taxes still apply, and this only works with the 401(k) from the employer you just left, not old 401(k)s or IRAs.

Risks of early withdrawal

Here are a few risks of early withdrawal:

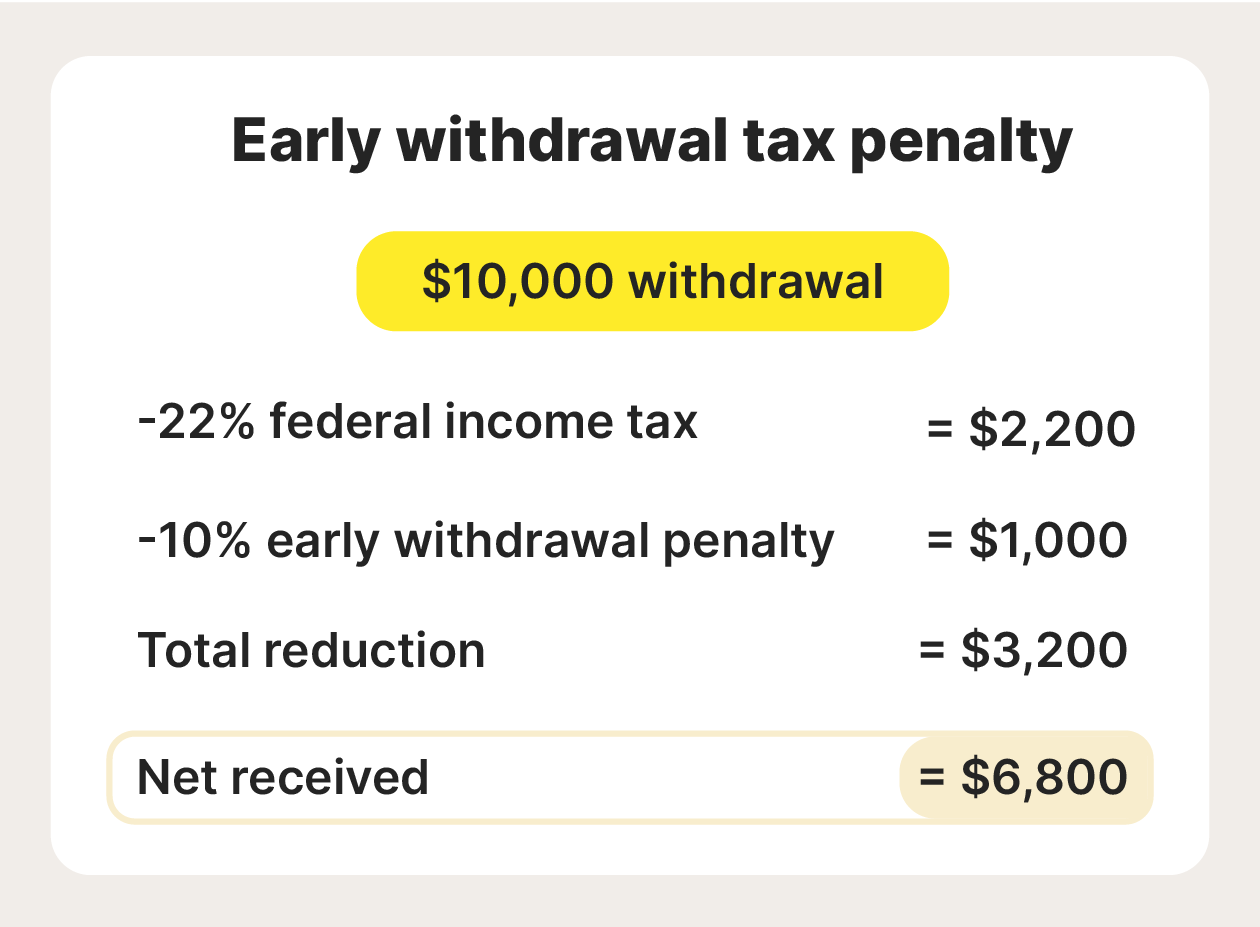

- Steep tax penalty: You’ll owe income tax plus a 10% penalty on the withdrawal, significantly reducing the amount you actually receive. A $10,000 withdrawal in the 22% tax bracket leaves you with only $6,800 after taxes and penalties.

- Permanent loss of retirement savings: Unlike 401(k) loans, withdrawals cannot be repaid, and you lose years of potential compound growth.

- Automatic tax withholding may not cover your full liability: Plans withhold 20% for federal taxes, but you may owe more at tax time depending on your total income.

- Reduced contribution room: You cannot “make up” the withdrawn funds later: annual contribution limits still apply.

- Potential state taxes: In addition to federal taxes and penalties, your state may also tax the withdrawal.

Top tip: Early 401(k) withdrawals are expensive. Between income taxes and the 10% penalty, you could lose 30-40% of your withdrawal to taxes.

Before taking an early withdrawal, explore alternatives like 401(k) loans, hardship withdrawals (if you qualify), or other funding sources. If you must withdraw, consult a tax professional to understand your total tax liability and whether you qualify for any penalty exceptions.

Cashing out your 401(k) means closing your account and withdrawing all the funds as cash. This option is typically only available after you leave your job. You generally cannot cash out a 401(k) while still employed with the company sponsoring the plan.

While cashing out provides immediate access to your money, it comes with significant tax consequences and permanently removes funds from your retirement savings. This option is often considered a last resort due to its long-term financial impact.

Here’s how you can cancel and cash out a 401(k):

- Locate your plan administrator: Contact your former employer, check old 401(k) statements, or search the Department of Labor's abandoned plan database to find your plan administrator's contact information.

- Request a distribution: Contact your administrator and request the distribution forms. You'll need to specify how you want to receive the funds (lump sum check, direct deposit, etc.).

- Submit your forms and confirm the transaction: Complete the required paperwork and verify that the funds have been transferred as requested.

What you need to know

When you cash out your 401(k), the entire amount is taxed as ordinary income in the year you receive it. If you’re under 59½, you’ll also owe a 10% early withdrawal penalty unless you qualify for an exception (such as the Rule of 55).

Your plan administrator will automatically withhold 20% for federal taxes. Furthermore, this may not cover your full tax liability. The additional income you receive from cashing out could push you into a higher tax bracket, increasing the taxes you owe on your entire annual income — not just the withdrawal.

Instead of cashing out, consider rolling your 401(k) into an IRA or your new employer's 401(k) plan. This preserves your retirement savings, avoids taxes and penalties, and keeps your money growing tax-deferred.

Risks of cashing out

Here are a few risks of cashing out your 401(k) early:

- Immediate tax hit: You’ll owe income tax on the entire withdrawal amount, plus a 10% penalty if you're under 59½.

- Potential bracket jump: The withdrawal could push you into a higher tax bracket, increasing taxes on your regular income.

- Permanent loss of retirement savings: Cashed-out funds cannot be replaced. You lose decades of potential compound growth.

- Withholding may fall short: The automatic 20% withholding often doesn't cover the full tax bill, leaving you with an unexpected liability at tax time.

- Lost creditor protection: Retirement accounts have strong legal protections from creditors in most states; cashed-out funds lose this protection.

Top tip: Cashing out your 401(k) should be a last resort. Between taxes, penalties, and lost compound growth, you could lose 30-50% of your account value and significantly compromise your retirement security.

Before cashing out, explore alternatives like rolling over to an IRA, taking a 401(k) loan, or leaving the money where it is. If you must cash out, consult a tax professional to estimate your total tax liability and plan accordingly.

Can I withdraw from my 401(k)?

You can withdraw from a 401(k) account, but early withdrawals are subject to restrictions, penalties, and tax implications. This is to prevent people from draining their retirement savings prematurely.

Before withdrawing, you should consult a financial advisor to understand the impact on your future financial security. Withdrawal rules vary based on the type of withdrawal you request.

Typical 401(k) withdrawal rules include:

- Age requirements: You must be at least 59½ to make withdrawals without the 10% early withdrawal penalty. Withdrawals before this age typically face both income taxes and a 10% penalty unless you qualify for an exception.

- Rule of 55: If you leave your job during or after the calendar year you turn 55, you can take penalty-free withdrawals from that employer's 401(k). Income taxes still apply.

- Hardship withdrawal restrictions: Some plans allow hardship withdrawals while you’re still employed, but only for an immediate and heavy financial need. You can withdraw only the amount necessary, and the funds cannot be repaid to the plan.

- Vesting requirements: You can only withdraw funds that are vested. This includes your own contributions (which are always 100% vested) and any employer contributions you’ve earned under your plan’s vesting schedule.

- Required minimum distributions (RMDs): Once you reach age 73, you’re generally required to start taking minimum distributions from your 401(k). But, if you’re still working for the employer sponsoring the plan and don’t own 5% or more of the company, you may be able to delay RMDs from that plan until you retire.

- Plan-specific rules: Your employer’s 401(k) plan determines which types of withdrawals are allowed, when you can take them, and what documentation is required. Not all plans permit withdrawals while you’re still employed.

Who do I contact to cash out my 401(k)?

To cash out your 401(k), you’ll need to contact the plan administrator or the financial institution holding your 401(k) account.

Here are your options for who to contact to cash out your 401(k):

- Find your plan administrator: Locate the plan administrator or HR department at your current or previous employer. They should have details on how to initiate a withdrawal.

- Contact the appropriate financial institution: If your 401(k) is managed by a financial institution (e.g., Vanguard, Fidelity, Charles Schwab), you can contact their customer service department.

Most financial institutions allow you to request a withdrawal by phone, through their website, or by mail. However, if your 401(k) is managed through a mobile-only banking app or digital platform (e.g., Chime, Robinhood), they may not offer direct customer service via phone — your only option may be to initiate the request through the app.

You will need to complete forms and verify your identity to ensure safe banking. Be prepared to provide necessary documents and possibly proof of your financial need if you’re claiming a hardship withdrawal.

Alternatives to 401(k) withdrawal

Because of the downsides of 401(k) withdrawals, it’s important to consider alternatives. Options like converting to an Individual Retirement Account (IRA) or taking a personal loan may help you preserve your retirement savings, avoid early withdrawal penalties, and maintain long-term financial growth.

- Stop contributing to your 401(k): If you’re struggling with short-term finances, consider temporarily halting contributions to your 401(k) to free up cash.

- Roll over to an IRA: Consider rolling your 401(k) into an IRA, as this allows you to maintain the tax-deferred growth of your retirement savings without incurring early withdrawal penalties or taxes. An IRA also offers a wider range of investment options than a 401(k).

- Withdraw from an emergency fund: If you have an emergency fund set up, it may be advisable to withdraw from this before requesting a 401(k) withdrawal to avoid penalties, taxes, and long-term consequences on your retirement savings.

- Take out a personal loan: If you need funds immediately, a personal loan means you can avoid tapping into your retirement savings and allow your 401(k) to continue growing. However, remember that interest rates on loans can vary based on your credit score.

- Get a home equity loan: A home equity loan or line of credit (HELOC) typically offers lower interest rates than personal loans or credit cards, but your home serves as collateral.

- Use your HSA savings for medical expenses: If you have a Health Savings Account (HSA), you can use it for eligible medical costs instead of requesting a hardship withdrawal.

- Use a 401(k) loan: Borrow from your 401(k) instead of withdrawing funds so you can pay yourself back with interest. You don’t incur taxes or penalties if repayments are made on time.

- Transfer high-interest debt to a lower-interest credit card: Moving balances from high-interest credit cards to cards with 0% or lower introductory interest rates can help you manage credit card debt without dipping into your retirement funds.

These options all have pros and cons, so it’s important to evaluate your financial situation and consult with a financial advisor before making a decision.

Get a clearer picture of your financial wellness

Withdrawing from a 401(k) involves considering and navigating methods like early withdrawals, hardship distributions, or loans. Each option has unique rules and risks, such as tax burdens, penalties, or diminished savings.

Managing these complex financial decisions requires strong financial awareness and fraud protection. With increasing threats of scams targeting retirement accounts, tools like Norton Money can provide added security, helping ensure you have a 360 degree view of your finances.

FAQs

When can I withdraw from a 401(k) for life events?

You can withdraw from a 401(k) at any age, but withdrawals made before age 59½ usually come with income taxes and a 10% early withdrawal penalty. However, the IRS allows penalty-free withdrawals in certain life-event situations, even if you’re under 59½. These exceptions are designed to help cover serious or unavoidable financial needs.

Common penalty-free exceptions include permanent disability, unreimbursed medical expenses that exceed 7.5% of your adjusted gross income (AGI), and qualified birth or adoption expenses.

When can I withdraw from a 401(k) without penalties?

The simplest way to avoid the 10% early withdrawal penalty is to wait until you reach age 59½. At that point, you can take distributions from your 401(k) without penalties, though withdrawals from a traditional 401(k) are still taxed as ordinary income.

There are also limited situations where you can withdraw before age 59½ without penalties. These include leaving your job during or after the year you turn 55 (the Rule of 55), qualifying for a hardship withdrawal under your plan’s rules, or withdrawing funds after your employer terminates its 401(k) plan without replacing it. Because eligibility and tax treatment vary, it’s important to confirm your options with your plan administrator and consult a financial advisor before withdrawing.

Editors’ note: Our articles offer educational information and are written to raise awareness about important topics in Cyber Safety. Norton products and services may not protect against every type of threat, fraud, or crime we write about. For more details about how we research, write, and review our articles, see our Editorial Policy.

Want more?

Follow us for all the latest news, tips, and updates.