15 bad financial decisions and how to avoid them

Bad financial decisions often start small, then quietly snowball into long-term money stress. From overspending to missed savings opportunities, these habits can drain your finances over time. Tools that help you monitor accounts, track spending, and protect your identity can make it easier to stay in control as you work toward healthier financial habits.

2025

Consumer

Security Innovator

- 1. Living beyond your means

- 2. Not having a budget

- 3. Failing to track expenses

- 4. Carrying a credit card balance instead of paying it off

- 5. Not having an emergency fund

- 6. Delaying retirement savings

- 7. Not using tax-advantaged savings accounts

- 8. Being uninsured

- 9. Waiting to invest

- 10. Failing to negotiate your salary

- 11. Wasting money on unused subscriptions

- 12. Not keeping track of your credit score

- 13. Overspending on a home

- 14. Buying depreciating assets

- 15. Not protecting yourself from identity theft

- Signs that you’re making a bad financial decision

- How to overcome a bad financial situation

- Manage your finances with Norton Money

- FAQs

Some bad financial decisions make headlines. Remember when Blockbuster passed on the chance to buy Netflix? Or when Beanie Babies convinced collectors they were sitting on retirement-level investments, only for the market to collapse?

Those stories are extreme, but they highlight a simple truth. Decisions that feel reasonable in the moment can age badly.

Financial mistakes can happen during everyday moments or during major life events. And when money feels tight, it becomes harder to plan ahead, save consistently, or spot risks early. This guide breaks down common examples of poor financial decisions, why they happen, and how to avoid repeating them.

1. Living beyond your means

Living beyond your means refers to consistently spending more than your income can comfortably support. Often, this happens when there’s no clear budget guiding your day-to-day financial decisions.

For example, grabbing an iced oat-milk latte with vanilla cold foam on the way to work every morning can quietly consume a large portion of your monthly income. Without defined limits, small, routine purchases can easily add up in ways that are hard to notice until the impact shows up in your bank account.

For example, people have shared how ordering takeout and taking an Uber home every day felt manageable. At least, until they looked at their bank account and realized how much of their paycheck was disappearing. When spending is automatic rather than intentional, saving and getting out of debt become harder.

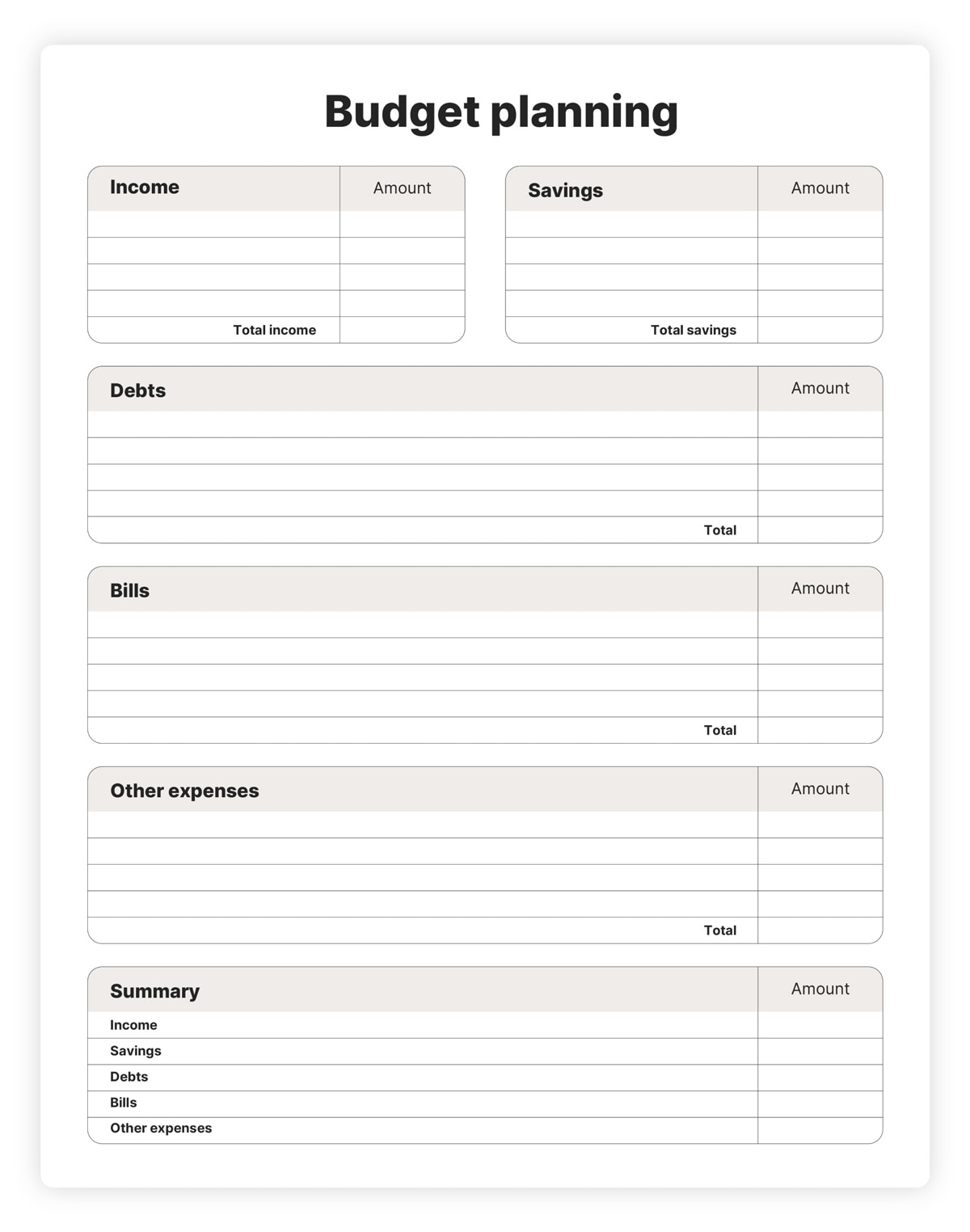

2. Not having a budget

Setting a budget helps you understand where your money’s going and how much you’ll have leftover at the end of each month. Without one, you may end up spending more money than you can afford or having to choose between important purchases.

Many people rely on mental estimates instead of written plans. But autopay charges, subscriptions, and irregular expenses make those estimates unreliable. A budget helps align spending with priorities, such as paying off credit card debt or building savings.

3. Failing to track expenses

Failing to track expenses makes it tough to understand where your money is actually going, which can lead to overspending even when it feels like you earn enough to cover everything. When spending happens without regular review, small purchases can quietly add up to hundreds of dollars.

This habit often shows up through forgotten or fragmented costs, including:

- Impulse buys.

- Automatic price increases on subscriptions or services.

- In-app purchases that seem small in the moment.

- Convenience charges related to travel, parking, or last-minute errands.

Without taking time to check your transactions, billing errors or unfamiliar charges can blend in with everyday activities instead of standing out as issues that need attention.

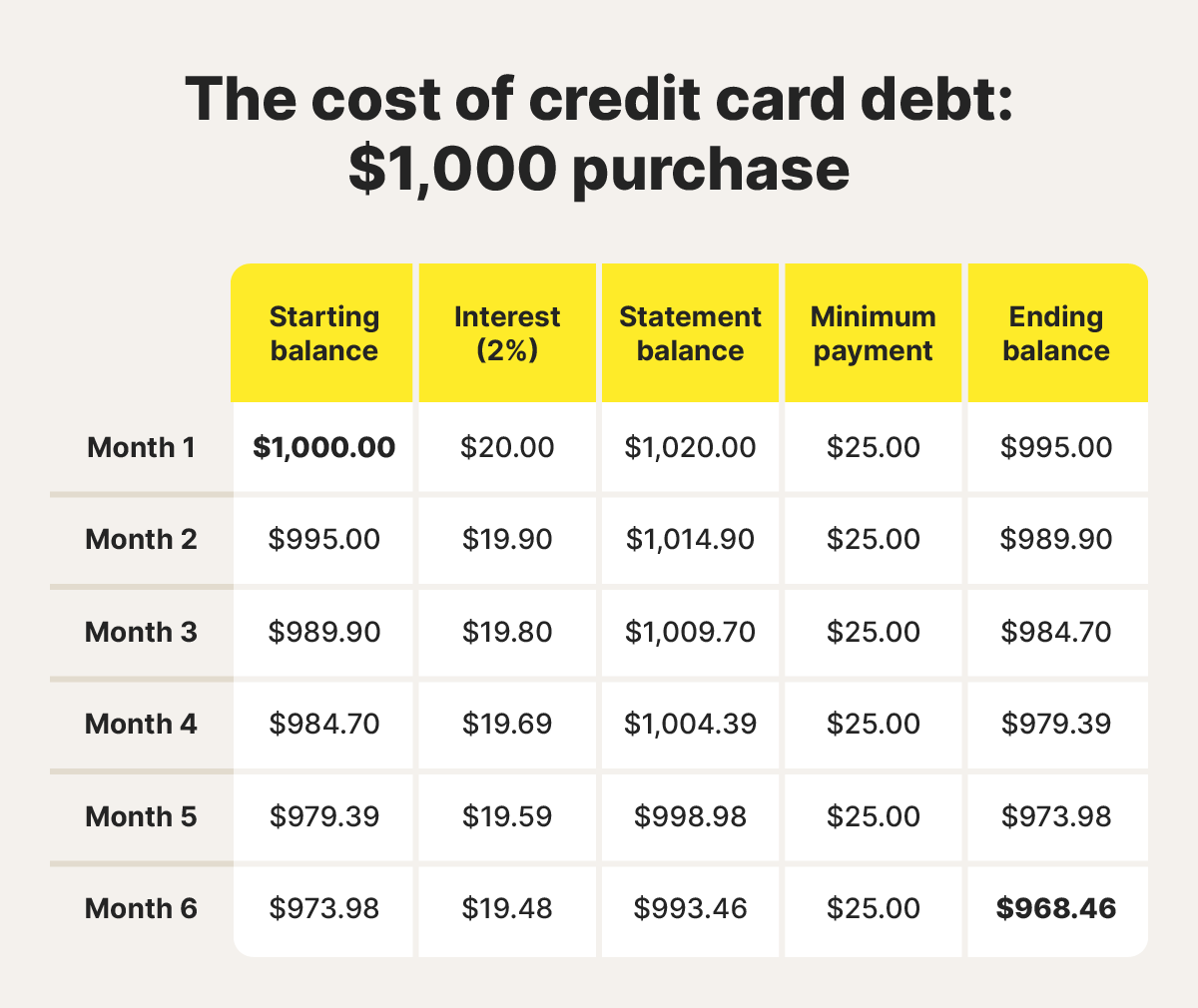

4. Carrying a credit card balance instead of paying it off

When you carry a credit card balance, you’re charged interest on what you owe. That interest is added to your balance, so the amount grows each month you don’t pay it off. Over time, even a small balance can quickly turn into a much larger debt.

When you make only the minimum payment, much of it usually goes toward interest instead of the original balance. The remaining amount keeps accruing interest, which slows your progress and makes it harder to pay off credit card debt. Over time, this can stretch out repayment for months or even years, leaving you with less money for savings or other financial goals.

High balances can also hurt your credit report and credit score. As your credit utilization increases, lenders may see you as a higher-risk borrower, which can lead to higher interest rates in the future.

5. Not having an emergency fund

While you cannot predict when an emergency will happen, you can plan for the financial impact. An emergency fund is money set aside specifically to cover unexpected expenses so they do not disrupt your budget or force you into difficult choices.

Costs like car repairs, last-minute travel, or medical bills often arrive without warning and sometimes at the same time. Without an emergency fund, people often have to cover these expenses with credit.

On Reddit, a user discussed a relatable bad financial situation where they had no emergency fund and had to buy last-minute plane tickets for a funeral while also paying for multiple car repairs. Nothing about their situation was avoidable, and it led to fast-growing credit card debt.

6. Delaying retirement savings

People often delay retirement savings because immediate expenses feel more pressing. When contributions are postponed, long-term goals like retiring early — or even on time — become much harder to reach.

When you postpone savings year after year, the timeline for building enough money to stop working comfortably can stretch out longer than expected.

Starting early gives your money more time to grow through compounding; waiting usually means needing to contribute more later to reach the same result.

Check whether your employer offers a retirement plan with matching contributions. Contributing enough to receive the full match ensures you take full advantage of the compensation that’s already part of your benefits package — effectively boosting your total pay without increasing your workload.

7. Not using tax-advantaged savings accounts

Tax-advantaged savings accounts are designed to help you keep more of your money by reducing the tax-burden on what you save or earn over time. Failing to make use of them often means paying more in taxes than necessary and slowing long-term progress.

Some people save exclusively in standard savings accounts because they feel comfortable and familiar, ignoring plans like health savings accounts (HSAs) even when eligible. The result is less efficient growth and higher lifetime tax costs.

8. Being uninsured

Being uninsured exposes you to financial risk that can be difficult to manage, even if you’re otherwise careful with money.

Health insurance is meant to limit how much you pay out of pocket when serious or unexpected medical care is needed. Without it, medical costs are often billed at full rates, which can swiftly overwhelm savings and disrupt long-term plans.

Without insurance, even brief hospital stays can lead to bills that take years to resolve. In one all-too-typical example, a Reddit user discussed waking up in a hospital after a head injury to a bill exceeding $32,000. They missed their enrollment window after changing jobs, and the financial stress followed long after the injury healed.

9. Waiting to invest

Investing supports long-term goals by allowing money to grow over time. But when people don’t know what to do or believe they need a lot of money to start investing, they may put it off.

Some people keep long-term savings parked in checking or savings accounts for years. A story on Reddit addressed a user’s regret of saving money in a bank instead of building wealth by investing earlier, realizing later how much growth they missed. Starting small and staying consistent matters more than perfect timing.

10. Failing to negotiate your salary

Many people don’t negotiate because it feels uncomfortable or they worry about rocking the boat. Others assume the first offer is the best they will get. But for many roles, employers expect negotiation and handle it professionally.

Doing a little homework ahead of time makes the conversation feel more manageable and puts you in a stronger position. To make sure you’re asking for an appropriate amount, look up salary ranges for the position and your experience level.

11. Wasting money on unused subscriptions

The average person spends around $200 per year on unused subscriptions. If you have multiple small monthly charges, they can take a significant chunk out of your budget before you know it.

Streaming services, fitness memberships, and beauty and snack boxes dip into your account every month, taking money that could otherwise go to savings or paying off debt. Audit recurring charges quarterly and cancel subscriptions you no longer use.

12. Not keeping track of your credit score

Your credit score influences everything from loan approvals and interest rates to housing and insurance decisions. When you are not monitoring it, you lose visibility into how lenders and other decision-makers see your financial profile.

Monitoring your credit regularly helps catch errors, outdated information, unauthorized accounts, and other issues early. It also lets you see whether changes like paying down balances or setting a budget are making a difference.

You can review credit reports from the three major credit bureaus once a week for free at annualcreditreport.com (the domain name is a misnomer). Staying aware makes it easier to protect your credit and avoid setbacks tied to fraud or simple reporting mistakes.

13. Overspending on a home

Housing costs are often the largest and most fixed part of a household budget. When too much income goes toward a mortgage, rent, property taxes, insurance, and ongoing maintenance, financial flexibility can shrink quickly, leaving little room to absorb surprises or save for other goals.

One Reddit user described homeownership as the worst decision they had made after spending more than $30,000 on repairs in just over two years. Experiences like this show how underestimating repair and maintenance costs can turn a stable purchase into a bad financial situation.

Likewise, if you find you’re paying too much in rent, consider moving to a less desirable neighborhood, getting a smaller apartment, or finding a roommate to help slash housing costs.

14. Buying depreciating assets

Depreciating assets are items that lose value over time instead of gaining it, meaning they are worth less the longer you own them. Cars are a prime example. They are often necessary, but overspending on them can slow financial progress in every other area.

In one such example of this kind of financial problem, an individual described the impact of buying a luxury SUV priced close to their annual salary. Making a bad financial decision like this causes payments to become a constant constraint, limiting savings and increasing reliance on credit.

15. Not protecting yourself from identity theft

Identity theft can affect your finances, credit, and even rob you of your time, as fraudulent accounts, unauthorized charges, and credit damage often take months to resolve.

Using a dedicated identity theft protection service like Norton 360 with LifeLock can also be a smart way to reduce this risk. LifeLock helps monitor for potential misuse of your personal information, alerts you to certain suspicious activity involving your identity, and provides restoration support if your identity is compromised, which can save you both money and time compared to handling fraud on your own.

Signs that you’re making a bad financial decision

Not every financial misstep is obvious in the moment. But certain red flags can signal that a decision deserves a second look, especially if it involves a large purchase or long-term commitment. Here are a few signs of a poor financial decision:

- You do not have a clear plan to pay off a purchase.

- Spending feels driven by impulse or emotion.

- You didn’t compare prices or alternatives on different sites.

- The expense doesn’t fit into your budget.

- You won’t have a financial cushion if something goes wrong.

- You feel rushed or pressured to make a decision.

How to overcome a bad financial situation

A bad money move doesn’t have to define your financial future. With a clear plan and steady habits, you can recover from a bad financial decision.

- Assess the impact: Take stock of your bank balance, income, interest rates on debt, payment deadlines, and any penalties. You can’t recover from a bad financial decision if you don’t know the extent of the problem.

- Stop additional damage: Pause unnecessary spending, cancel unused subscriptions, and avoid taking on new debt.

- Prioritize high-interest debt: If debt is involved, focus extra payments on the highest-interest balance first while maintaining minimum payments on others.

- Create a short-term recovery plan: Sit down in front of a spreadsheet and plan specific actions for the next 30 to 90 days, such as cutting certain expenses, reallocating savings, or working overtime.

- Communicate with lenders early: Many lenders offer hardship options, modified payment plans, or temporary relief.

- Put guardrails in place: Automate savings, track expenses weekly, or use budgeting tools like Norton Money to help reduce friction, get visibility into your spending habits, and prevent repeat mistakes.

- Shift your mindset: View the experience as a learning moment rather than a permanent setback. Financial progress comes from learning and adjusting after making mistakes.

Manage your finances with Norton Money

Managing your finances involves more than just budgeting. Tools that monitor your accounts and credit activity can support healthier money habits as you work toward your financial goals.

Norton Money helps bring your financial information into one place, giving you an eagle-eye view of your spending and credit activity. Having that visibility allows you to spot problems sooner and take action before small issues turn into larger issues.

FAQs

What is the $27.40 rule?

The $27.40 rule is a simple savings strategy designed to help you set aside $10,000 in a year by saving about $27.40 per day ($10,000 divided by 365 days). By breaking a large goal into manageable daily amounts, it encourages consistent micro-saving — often limiting daily discretionary spending like takeout, subscriptions, or impulse purchases.

How to recover from a bad financial situation?

Starts by reviewing your income, fixed expenses, and discretionary spending to understand exactly where your money goes. From there, prioritize paying down high-interest debt and begin building an emergency fund, even if you start small. Consistent, incremental changes can compound into meaningful progress over time.

Why do I keep making bad financial decisions?

Financial missteps often stem from stress, ingrained habits, or limited visibility into your spending. When decisions are reactive instead of intentional, patterns repeat. Increasing awareness through budgeting tools, spending reviews, or automated savings, and reducing friction around good habits can help you break the cycle and regain control.

Editors’ note: Our articles offer educational information and are written to raise awareness about important topics in Cyber Safety. Norton products and services may not protect against every type of threat, fraud, or crime we write about. For more details about how we research, write, and review our articles, see our Editorial Policy.

Want more?

Follow us for all the latest news, tips, and updates.