What are credit score ranges? Learn the good and bad credit tiers

The credit range you fall into shows lenders how likely you are to repay loans and credit. Being in the exceptional, very good, or good credit score ranges can help you secure better credit terms. This guide breaks down each range, what affects them, and how Norton Money can help you build healthier financial habits.

2025

Consumer

Security Innovator

Your credit score influences more than loan approvals — it can affect interest rates, rental applications, insurance premiums, and even job screenings. Understanding where you stand today gives you leverage tomorrow. Let’s take a closer look at how the scoring system works and what it means for your financial opportunities.

Understanding credit score ranges

When it comes to credit, you’re not just “approved” or “denied” — there are different credit score levels that lenders use to understand your financial reliability and tailor their offerings. Each tier is defined by a specific credit score range and labeled from exceptional to poor.

Why does this matter? Because your credit score range level has a major influence on your approval odds for credit cards or mortgages, the rate you’ll receive on loans, and your overall financial flexibility. Knowing where you sit on the credit score range chart and what a good credit score range is can help you secure better rates. Striving for the top tiers can reduce borrowing costs and unlock stronger long-term financial opportunities.

For context: in the U.S., the average FICO® Score was 715 in 2025, which places the average consumer solidly within the Good credit range.

In the sections that follow, we’ll describe each credit score level, demystify how scoring works, and show you how to set financial goals to move into stronger tiers. All ranges below are based on the FICO model, but note that other credit score models are widely used, too.

Level 1. Exceptional credit

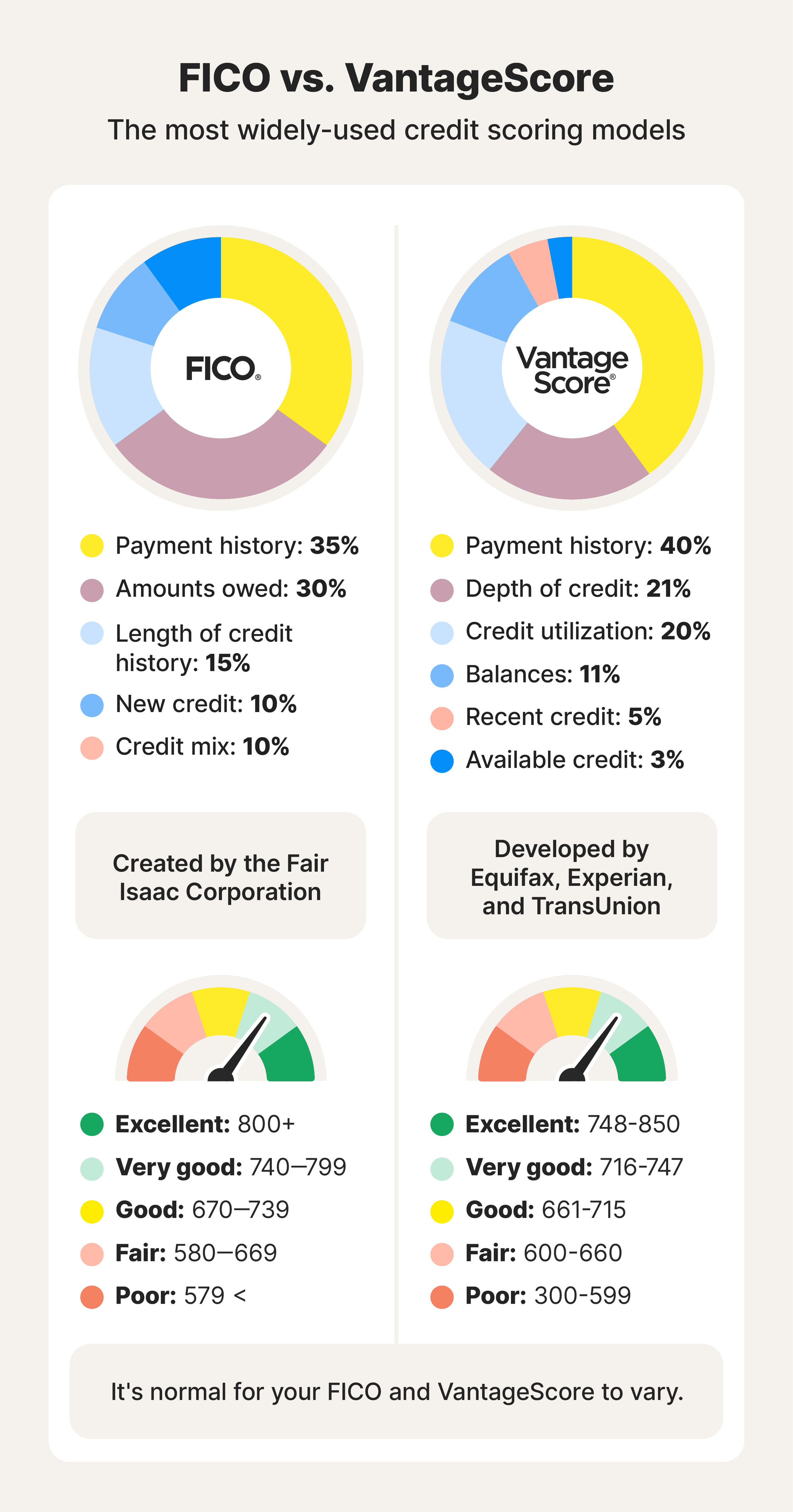

The highest tier in the FICO model is “Exceptional” credit (sometimes referred to as “Excellent”) and typically falls within the 800–850 range. This is the top range of all credit score models, and is the level you should ultimately aim for, as it represents the strongest overall credit score ratings and the lowest risk to lenders.

Being in this credit score tier means you’ll generally receive the best credit offers available: the lowest interest rates, the highest approval odds, premium credit card options, stronger negotiating power, and access to top-tier lending products. In short, the Exceptional credit range gives you maximum financial flexibility and long-term savings across all major borrowing decisions.

Level 2. Very good credit

The “Very good” credit score range sits just below Exceptional, between 740–799 on the FICO scale. This is the second-highest range, signalling to lenders that you are a low-risk, consistently reliable borrower with a strong financial track record.

With a score in this Very good range, you’ll generally qualify for most lenders’ best or near-best offers, including competitive interest rates, access to premium credit cards, and smoother approvals for mortgages, auto loans, and personal loans.

Level 3. Good credit

The “Good” credit score range typically falls between 670–739 in the FICO model. In 2025, the average FICO score for Americans was 715, which falls within this range.

A Good credit score rating is what generally signals to lenders that you’re a dependable borrower who qualifies for most mainstream credit products. While you may not receive the lowest interest rates, a Good credit score number still offers solid approval odds and a strong base to build toward higher tiers over time.

Level 4. Fair credit

The “Fair” credit score range typically falls between 580–669 in the FICO model. This is one of the lower levels within the credit score ranges, but if you fall into this category, no need to panic — there are several ways to improve your credit score, as long as you work steadily.

Being in the Fair band indicates higher risk to lenders, which can result in higher interest rates, smaller loan approvals, or additional fees. While you may still be able to access credit, the terms are generally less favorable at this level.

Level 5. Poor credit

The “Poor” credit score range in the FICO model falls below 580. This is the lowest tier on the 300–850 FICO scale, and improving beyond this range significantly expands access to credit and lower borrowing costs.

Being in this range can make it difficult to qualify for loans, credit cards, or competitive interest rates. Consumers in this tier often face higher borrowing costs and stricter approval standards. Missed payments, high balances, or other bad financial decisions commonly contribute to a Poor credit score. Taking steps to build credit responsibly can help move your score into a higher, healthier range over time.

Different credit score models

Multiple credit scoring models exist, which is why your credit score range can vary depending on the system being used. The most widely used model in the U.S. is FICO®, and its 300–850 scale is the benchmark most lenders rely on.

Other scoring models — like VantageScore, developed by the three credit bureaus — use different methodologies, resulting in slight variations between score ranges.

Many consumer platforms provide VantageScore 3.0 or other educational scores to help people monitor their credit health. While these scores are valuable for tracking progress, lenders may use different models when making lending decisions. A credit scores and reports tool can also offer a helpful credit score breakdown, but lenders may not use them for approvals.

Key differences across credit scoring models often include:

- The factors they consider (for example, payment history and total debt).

- The weighting used in the breakdown (some models may prioritize credit age, while others may weigh utilization more heavily).

- How long they require an account to be open before generating a score (FICO requires more history than VantageScore, for example).

Here’s a detailed look at how credit scores range from model to model.

FICO

The FICO model was created by the Fair Isaac Corporation and is the most widely used scoring system in the US. Because lenders rely heavily on it, FICO score ranges can strongly influence approvals, interest rates, and loan terms.

The standard FICO credit score range spans 300–850, and is measured using five main categories:

- Payment history (35%): Evaluates whether you’ve paid past credit accounts on time. Late or missed payments lower your score, while consistent, timely payments help improve it.

- Amounts owed/credit utilization (30%): Measures how much debt you have relative to your available credit. Higher balances and utilization can signal financial strain and greater financial risk to lenders.

- Length of credit history (15%): Considers how long your credit accounts have been open. Older accounts demonstrate long-term reliability, while short histories can contribute to limited movement into higher credit score ranges.

- New credit (10%): Opening multiple accounts in a short period may indicate risk. Hard inquiries and rapid borrowing can temporarily lower your FICO score and keep you in a low credit range.

- Credit mix (10%): A healthy blend of credit types, such as credit cards or installment loans, can help improve your score if managed responsibly.

FICO also includes FICO Industry-Specific Scores, tailored versions used for auto loans, credit cards, and mortgages. These apply different chart ranges and weightings to better predict risk within each lending category.

VantageScore

VantageScore was developed collaboratively by the three major credit bureaus — Experian, Equifax, and TransUnion — to provide a unified scoring model. Because it uses its own formula and weighting, your VantageScore may differ slightly from your FICO score.

Just like FICO, VantageScore 3.0 and 4.0 use the 300–850 scale, while earlier versions (VantageScore 1.0 and 2.0) used a 501–990 scale

VantageScore 3.0 is widely used by consumer-facing platforms and financial institutions, including for some credit monitoring services and some prequalification processes. However, lenders may use different scoring models depending on the type of credit you apply for.

A VantageScore 3.0 credit score is measured using these five categories:

- Payment history (40%): Evaluates consistent, on-time payments and your ability to demonstrate reliability; late payments can quickly reduce your credit score and overall credit score range.

- Depth of credit (21%): Refers to the history and variety of credit types. Older, varied credit history signifies financial stability. Short histories or limited account types may make it harder to rise on the credit score scale.

- Credit utilization (20%): VantageScore 3.0 reviews how much of your available credit you use. Lower utilization (generally 30% utilization or lower) is regarded as more responsible borrowing.

- Balances (11%): High outstanding balances across credit lines may indicate potential repayment challenges and can contribute to lowering your overall credit score and range.

- Recent credit (5%): Multiple applications or new accounts in a short period may signal risk. Hard inquiries can temporarily lower your range until your account activity stabilizes.

- Available credit (3%): Refers to the amount of credit available for utilization. The higher the available credit and the lower the utilization, the better.

Implications of a bad credit score range

A bad credit range generally covers the Poor–Fair levels of credit score ratings, where lenders see you as representing a higher risk. Being in this range can limit your financial options and increase your rates on loans, credit cards, insurance, and even utilities.

Key implications of a bad credit range include:

- Higher interest and borrowing costs, making everyday credit more expensive.

- Increased difficulty getting approved for mortgages, personal loans, and premium credit cards.

- Lower credit limits and stricter repayment terms.

- Potential issues renting an apartment or securing certain jobs that review credit history.

If you fall into a lower credit range, stay alert to scams targeting people seeking fast fixes. Fraudsters may spoof legitimate companies and promote credit repair scams promising guaranteed improvements. Beware of fake tradeline services claiming to boost scores instantly and debt settlement scams that charge high fees and worsen your situation.

Always research before signing anything, and if you're concerned about identity abuse or suspicious activity, you can freeze your credit report to block unauthorized access while rebuilding your financial footing.

How to get your credit score

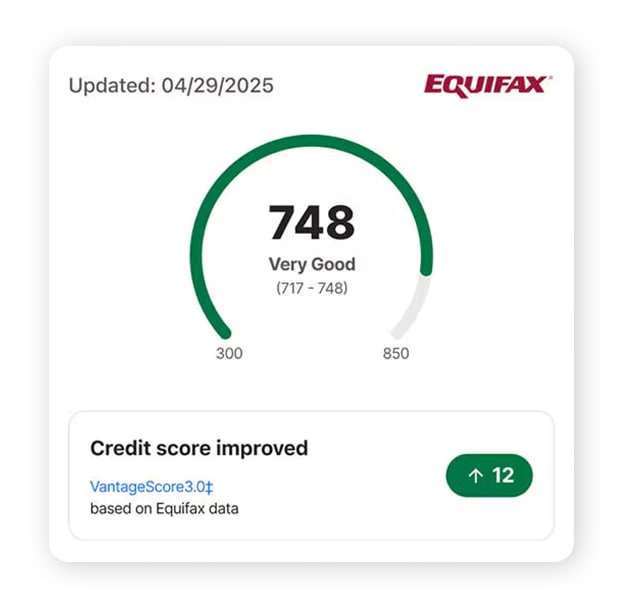

You can check your credit score through your credit card issuer, lender, or a trusted credit monitoring and financial wellness service like Norton Money. These tools display your current score and range, though the exact number may vary depending on the scoring model used. For example, Norton Money shows your VantageScore 3.0, which is the model used by Equifax and the other credit bureaus.

You can check your credit score as often as you like — it won’t impact your credit score range or lower your score. Regular checks help you stay aware of changes and catch inaccuracies early.

How to improve your credit score range

Whether you’re currently sitting in a lower tier or trying to maintain your strong credit score range, improving your overall credit score helps unlock better rates and long-term financial stability.

Here are a few ways to improve your credit score:

- Pay bills on time: Payment history is one of the biggest factors in shaping your score, whether it’s FICO or VantageScore 3.0.

- Reduce your balances: Getting out of debt lowers your credit utilization ratio, which can quickly boost your rating.

- Stay on top of your expenses: Tracking your expenses can help you set a budget, make payments on time, and keep credit utilization lower.

- Avoid closing old accounts: Older accounts help maintain a longer credit history, which contributes to a higher credit score.

- Limit new credit applications: Each hard inquiry can temporarily dip your score, so apply only when necessary.

These small habits compound over time, helping your credit score trend upward and stay strong.

Build your credit score with Norton

Understanding your credit score levels helps you see where you stand. Falling into a lower level can mean higher interest rates, fewer approvals, and added financial stress — while landing in a good or exceptional range opens doors to better finances.

Improving your credit takes consistency: paying on time, lowering debt, and monitoring your profile for changes or errors. That’s where Norton Money can help. With built-in tools for expense and credit score tracking, Norton Money gives you the visibility and alerts you need to stay on top of your score and keep it moving in the right direction.

FAQs

What is a good credit score to buy a house?

Most conventional mortgage lenders require a minimum credit score of around 620 to qualify. But higher scores greatly increase your chances of approval and access to favorable mortgage rates.

What is a good credit score to buy a car?

Aiming for a credit score of 670 or higher can improve your chances of qualifying for better car loan terms. For auto loans in particular, higher scores typically translate to lower interest rates. While some lenders may approve applicants with Fair or even Poor credit, those loans often come with significantly higher APRs (annual percentage rates), increasing the overall cost of borrowing.

What is a good credit score by age?

There are no official credit score targets by age, since scores depend on credit history length and responsible usage rather than demographics. Many people aim for 700+ by their 30s or 40s to maximize financial options.

How rare is a 700 credit score?

A 700 credit score isn’t particularly rare. The U.S. average credit score in 2025 was around 715, so having a 700 is fairly common and considered solidly in the Good range by most lenders.

Is a 900 credit score possible?

No. Current mainstream credit models cap at 850. A score of 900 isn’t attainable under these systems.

Editors’ note: Our articles offer educational information and are written to raise awareness about important topics in Cyber Safety. Norton products and services may not protect against every type of threat, fraud, or crime we write about. For more details about how we research, write, and review our articles, see our Editorial Policy.

Want more?

Follow us for all the latest news, tips, and updates.